Our Mission: Empower Do-It-Yourself Investors with Free Academic-based Research & Resources for Life-long Investing

Market got you down? How to construct a comeback portfolio

Reprinted courtesy of MarketWatch.com.

Published: March 26, 2020

To read the original article click here

Millions of investors are understandably upset about this month’s volatility in the stock market. After a decade of unusually favorable returns, the market has suddenly dished out a harsh dose of reality.

If you’re among these troubled investors, there are three things I think you should do.

First, do nothing immediately. Your emotions and gut reactions aren’t likely to do you any favors. This is a time to figure it out and get it right.

Second, calm your emotions enough to get some perspective. Yes, you may have lost a lot of money in the past few weeks. But it’s probably not the end of the world.

Third – and this is the topic here — remodel your portfolio for a strong comeback.

Obviously, nobody can tell you when the markets will start a lasting recovery. Probably not right away, though you never know. But if history is any guide, we won’t get much advance notice.

If you’re feeling stock-market pain right now, the two most likely causes are:

- You’re in over your head in terms of risk, holding too much of your portfolio in equities.

- You’re inadequately diversified, counting too much on one or two asset classes.

I recently wrote about that first point, and I don’t need to repeat it here except to emphasize how important this is. Check it out here.

What I’m advocating to address the second point above is not a cure-all for the market trouble we’re suddenly in. When the markets implode, there’s no thoroughly safe hiding place (except perhaps cash).

But if you want to build a strong comeback portfolio, with history on your side, it’s not hard to do.

It doesn’t require any complicated assets or contracts. No hocus-pocus or get-rich-quick claims. You can start with just four low-cost index funds in four tried-and-true types of U.S. stocks, in equal measures.

Simplicity itself.

In this article, I’ll outline my recommendations, then give you the statistical evidence to support them, and finally make specific suggestions for carrying out this plan.

The building blocks

Start with the S&P 500 index , the most common proxy for the U.S. stock market. Lots of people think you could start and end your portfolio right there — and for many investors that might be enough.

But twice in just the past 20 years, the S&P 500 has dealt out losses of over 50% (the technology tumble of 2000-2002 and the real estate collapse of 2007-2008). For true peace of mind, you should have something more.

Still, this broad market index compounded at nearly 10% for the past 92 calendar years — through world wars (hot and cold), depressions, recessions and all manner of crises.

The S&P 500 is a good workhorse, so to speak, and it makes up 25% of the comeback portfolio I’m recommending.

Building block No. 1: An index fund representing this index.

The S&P 500 represents large-cap blend stocks; blend indicates a combination of value stocks and the more popular growth stocks.

The other three asset classes that I’m prescribing have outperformed the S&P 500 over the past 90 years.

The second 25% of my recommended portfolio is large-cap value stocks. Value stocks (both large-cap and small-cap) have a strong track record of outperforming growth stocks over the long haul, though not in every single year or every decade.

Building block No. 2: A large-cap value index fund, which will tilt your equity portfolio toward value stocks.

The second half of your portfolio mirrors the first, only concentrating on small-cap stocks, which have outperformed large-cap stocks over the decades.

Building block No. 3: A small-cap blend index fund.

Building block No. 4: A small-cap value index fund.

With equal weightings in those four funds, you will be set up to capture a piece of the action, whether the market leaders are small-cap stocks or large-cap ones, and whether growth stocks or value stocks are outperforming at any given time.

These four funds will keep your assets in U.S. stocks, which many people find more comfortable than international stocks.

Here’s why that matters: The more comfortable you are with your portfolio, the more likely you are to stick with it — and reap its long-term rewards.

(Of course, the same thing could be said about a poorly chosen portfolio that’s comfortable. So it’s important to understand the reasons for choosing what you do.)

The evidence

Reliable data going back to 1928 gives us 92 years of returns for these four asset classes. Here are some numbers to support my recommendation of diversifying beyond the S&P 500.

The S&P 500 index had a compound return of 9.9% over those 92 years.

You are unlikely to have an investment horizon that long. But most investors can look ahead at least 15 years. In the 77 15-year periods from 1928 through 2019, the S&P 500 on average compounded at 10.7%. Over 40-year periods (there were 52 of them), the index compounded at 11%.

Large-cap value stocks compounded at 11.1% over 92 years and at 12.9% in the average 15 year period, 13.5% over the average 40-year period.

Small-cap blend stocks: 12% from 1928 through 2019, 13.6% in the average 15 year period, and 13.8% over the average 40-year period.

Small-cap value stocks: 13.2% from 1928 through 2019, 15.8% in the average 15 year period, and 16.2% over the average 40-year period.

When you put these four asset classes together in equal measures as I’m recommending, assuming annual rebalancing, here are the comparable numbers:

Over 92 years, the compound return was 11.8%; in the average 15-year period, 13.4%; in the average 40-year period, 13.8%.

You’ll find these numbers and more details in this table.

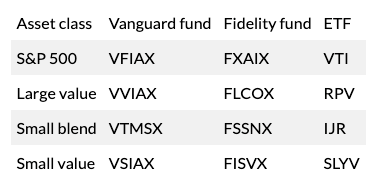

The specific funds

It’s easy to put this comeback portfolio together. Here are my specific best-in-class recommendations for index funds and no-commission ETFs at Vanguard and Fidelity.

This four-asset-class portfolio was featured in an article I wrote just two months ago when optimism was running rampant. Check it out here, and you’ll find some colorful tables showing how this combination fared over the past nine decades.

My latest podcast, “How to build the best comeback portfolio,” covers more details of this recommendation.

Richard Buck contributed to this article.

Delivery Method. Paul Merriman will send stories to MarketWatch editors on a biweekly basis. Licensor may republish such stories 24 hours after publication on MarketWatch with the attribution.